Global Polysilicon Market to Reach USD 44.7 Billion by 2035 as Solar PV Expansion and Semiconductor Demand Accelerate Growth

Driven by n-type solar cell adoption, utility-scale photovoltaics, and ultra-high purity semiconductor applications, polysilicon demand surges across renewable energy and advanced electronics value chains.

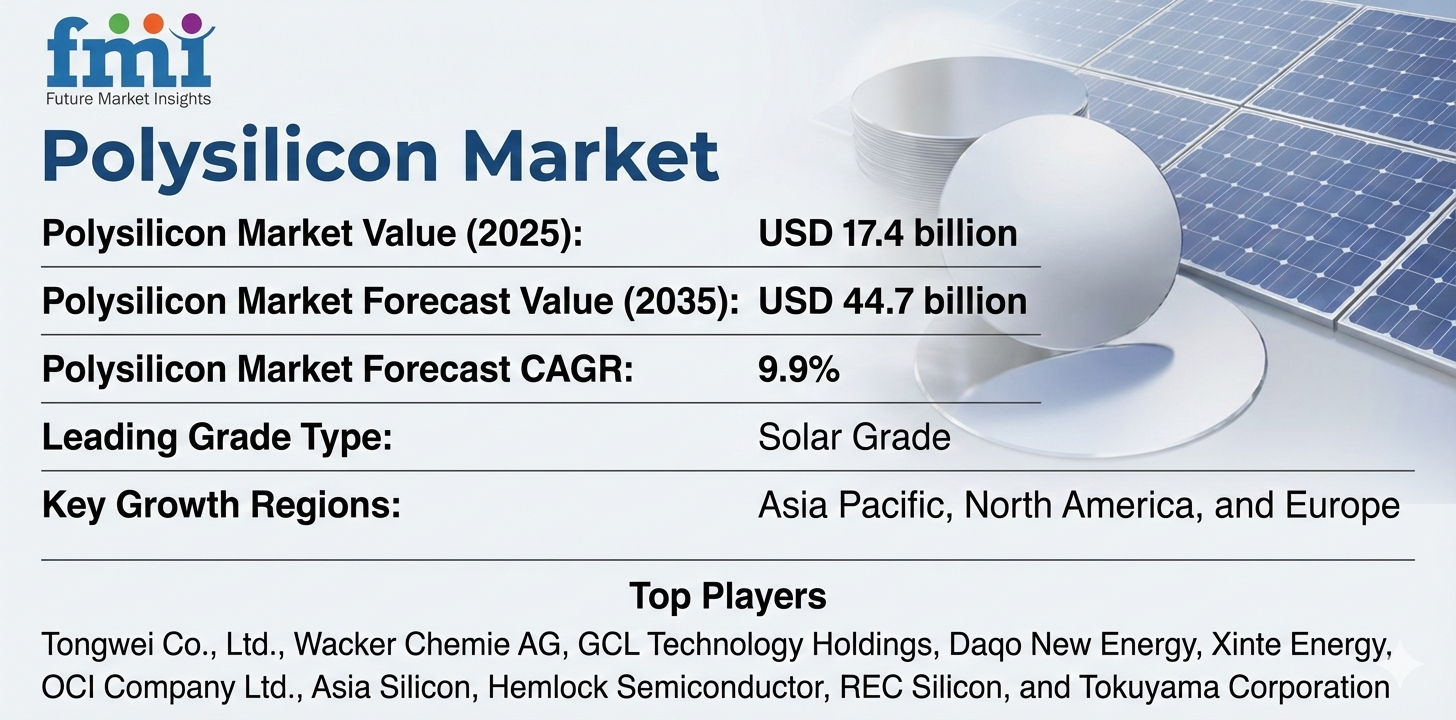

NEWARK, DELAWARE / ACCESS Newswire / February 11, 2026 / The global polysilicon market is entering a decade of sustained expansion, projected to grow from USD 17.4 billion in 2025 to USD 44.7 billion by 2035, according to a new outlook by Future Market Insights (FMI). This trajectory represents a strong 9.9% CAGR, underpinned by accelerating deployment of solar photovoltaic systems, rising semiconductor manufacturing capacity, and rapid adoption of advanced n-type solar cell technologies including TopCon and heterojunction (HJT).

Polysilicon remains the foundational material for crystalline silicon solar cells and semiconductor wafers, positioning it at the center of the global energy transition and digital infrastructure buildout. Asia Pacific leads production and consumption, supported by integrated solar manufacturing ecosystems in China and emerging capacity in India, while North America and Europe continue to anchor demand through solar deployment and electronics-grade applications.

As governments worldwide intensify renewable energy commitments and semiconductor localization strategies, polysilicon is evolving from a commodity input into a strategic material critical for clean power generation and advanced electronics manufacturing.

Solar Grade Polysilicon and Energy Applications Form the Market Backbone

Solar-grade polysilicon dominates the global market, accounting for approximately 79.0% of total demand, reflecting its widespread use in photovoltaic ingot, wafer, and cell production. These materials support high-efficiency mono-PERC, TopCon, and HJT architectures, enabling module manufacturers to meet increasingly stringent performance standards while maintaining cost competitiveness.

Solar PV cells and modules represent the largest end-use segment, contributing nearly 86.0% of total consumption. Utility-scale solar farms, commercial rooftop installations, and residential systems continue to drive material demand as countries pursue grid decarbonization and energy security objectives.

Electronics-grade polysilicon maintains a significant 21.0% share, serving semiconductor fabrication facilities that require ultra-high purity feedstock for logic, memory, and power devices. Expansion of 300mm wafer production and advanced chip manufacturing supports steady growth from electronics applications.

"Polysilicon has become indispensable wherever efficiency, purity, and scalability converge," notes the FMI analysis. "From gigawatt-scale solar farms to precision semiconductor fabs, polysilicon enables both energy transition and digital transformation."

Renewable Energy Deployment and Manufacturing Innovation Drive Consistent Adoption

Global demand for polysilicon continues to strengthen as industries respond to climate targets, electrification trends, and technology modernization:

Solar PV Expansion: Rising utility-scale and rooftop solar installations drive sustained demand for solar-grade polysilicon.

N-Type Cell Transition: Manufacturers increasingly adopt TopCon and HJT technologies requiring higher-purity feedstock.

Semiconductor Capacity Growth: Logic, memory, and power electronics fabrication fuels demand for electronics-grade polysilicon.

Production Technology Advances: Siemens process optimization, fluidized bed reactors, and purification improvements enhance efficiency and reduce costs.

However, the industry faces challenges including raw material price volatility, regional production overcapacity, and the energy-intensive nature of polysilicon manufacturing. In response, producers are investing in renewable-powered facilities, efficiency upgrades, and sustainable production models to align with global ESG expectations.

Regional Growth Engines: Asia Pacific Accelerates, India Emerges as Fastest-Growing Market

The polysilicon market is expanding globally, led by Asia Pacific, with China maintaining manufacturing leadership and India emerging as the fastest-growing national market.

Country | Projected CAGR | Primary Growth Drivers |

|---|---|---|

India | 14.2% | Solar manufacturing buildout, utility-scale PV, domestic incentives |

China | 10.5% | Integrated PV value chains, n-type adoption, export manufacturing |

Spain | 7.0% | Utility-scale solar deployment, renewable auctions |

Saudi Arabia | 6.1% | Renewable mega-projects, Vision 2030 programs |

United States | 5.3% | Solar supply chain localization, semiconductor expansion |

India's rapid growth is supported by production-linked incentive schemes, large-scale solar tenders, and integrated photovoltaic manufacturing initiatives. China continues to dominate global output through vertically integrated ingot-to-module operations and advanced n-type technology leadership.

The United States sustains demand through utility-scale solar deployment and semiconductor reshoring, reinforced by Inflation Reduction Act incentives. Europe, led by Germany and Spain, benefits from distributed solar adoption and electronics-grade purification capabilities.

Sustainability and Regulatory Alignment Shape Market Evolution

Despite strong growth fundamentals, the polysilicon industry faces increasing scrutiny over carbon footprint and energy consumption. Environmental compliance requirements across Europe and North America are accelerating innovation in low-carbon production methods.

Key industry focus areas include:

Development of renewable-powered polysilicon facilities

Advanced purification and contamination control systems

Energy-efficient Siemens and FBR production technologies

Circular economy initiatives and silicon recycling pathways

Long-term scalability depends on balancing production capacity with downstream solar and semiconductor demand while improving sustainability metrics across manufacturing operations.

Competitive Landscape and Market Dynamics

The global polysilicon market remains moderately consolidated, with the top five producers controlling approximately 70-75% of total supply. Market leaders benefit from advanced production technologies, large-scale capacity, and deep integration with solar and electronics value chains.

Competition increasingly centers on material purity, manufacturing efficiency, sustainability credentials, and long-term supply reliability rather than volume alone. Producers are expanding capacity to support next-generation solar architectures while advancing cleaner processes to meet tightening environmental standards.

Key Players in the Polysilicon Market

Tongwei Co., Ltd.

Wacker Chemie AG

GCL Technology Holdings

Daqo New Energy

Xinte Energy

OCI Company Ltd.

Asia Silicon

Hemlock Semiconductor

REC Silicon

Tokuyama Corporation

These companies continue to invest in ultra-high purity production, vertical integration strategies, and low-carbon manufacturing to strengthen positioning across solar and semiconductor applications.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Polysilicon Market through 2035, visit the official report page at: https://www.futuremarketinsights.com/reports/polysilicon-market

Related Reports:

Polyether Modified Polysiloxane Market: https://www.futuremarketinsights.com/reports/polyether-modified-polysiloxane-market

Polyethersulfone (PES) Market: https://www.futuremarketinsights.com/reports/polyethersulfone-market

Polyetheramine Market: https://www.futuremarketinsights.com/reports/polyetheramine-market

Polyetherimide (PEI) Market: https://www.futuremarketinsights.com/reports/polyetherimide-pei-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

Information contained on this page is provided by an independent third-party content provider. XPRMedia and this Site make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact [email protected]